Max writes*

The global strain of public debt crossed $100 trillion at the end of 2020. While developing countries account for a fraction of this sum, they face the highest risk of debt distress due to higher financial scrutiny. This enforces a feedback loop that does little to stimulate their growth or development. The growing financialization of environmental goods in recent years has offered a promising lifeline for developing countries endowed with nature reserves in the form of “debt for nature” swaps (DFNs). As the name suggests, a debtor is granted a discount on their debts in exchange for a commitment to conservancy. In the 2021 case of Belize, this meant a 12% nominal reduction in public debt. The benefits to the debtor are clear-cut but what do the creditors stand to gain?

In recent years, the parties involved in DFNs expanded from rich creditor governments to include commercial bondholders. In line with the growing popularity of environmental, social, and governance (ESG) in recent years, investors are jumping on these deals with an eagerness to tap new sources of income. They are interested because of a new potential for financial returns. To get a better understanding of how investors get their money’s worth, the case of Belize will be analyzed.

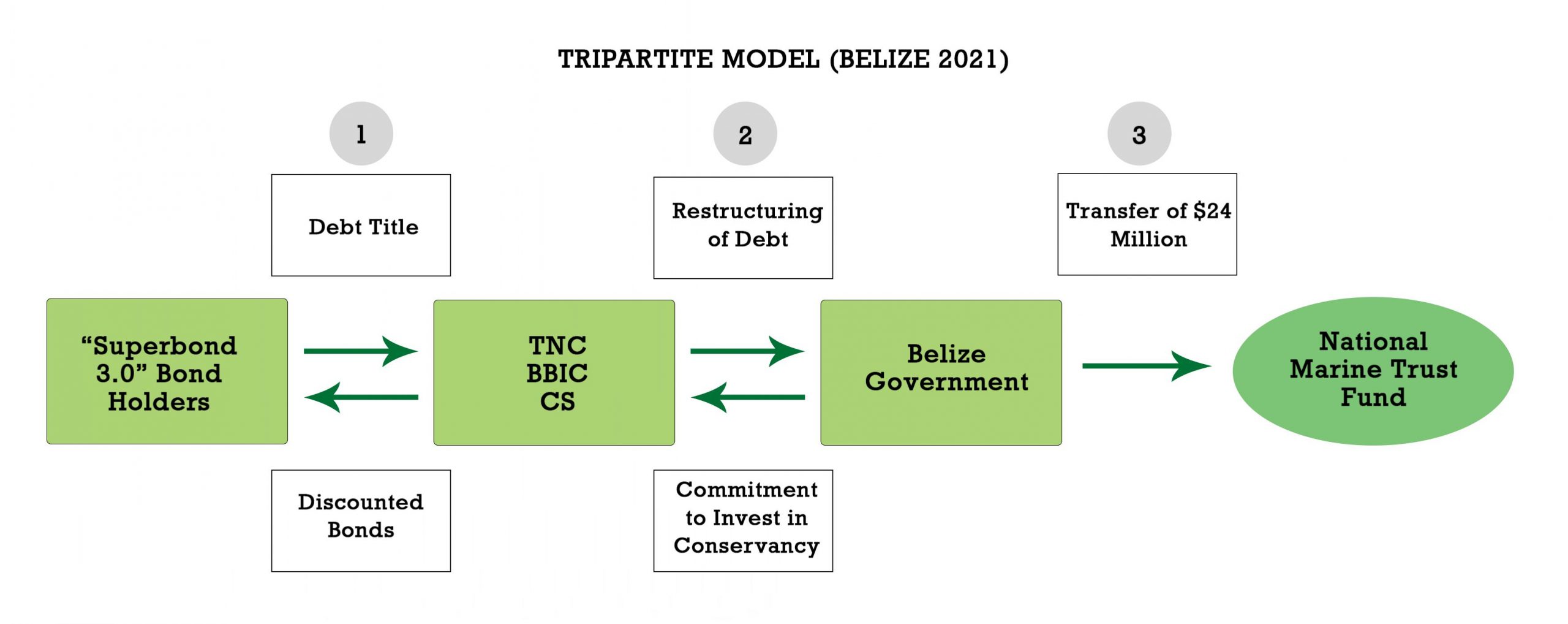

The DFNs were facilitated with the help of The Nature Conservancy (TNC), a US-based environmental NGO, the Belize Blue Investment Company (BBIC), which is a subsidiary of TNC, and Credit Suisse (CS), referred to as the “middlemen” from now on. The deal assumed a tripartite model wherein the middlemen paid off the bondholders of the “Superbond 3,” which in 2021 was trading 40% below its face value and carried high default risk. On the secondary market, the bondholders were willing to accept the 40% discount because it was better than a default.

The DFNs were facilitated with the help of The Nature Conservancy (TNC), a US-based environmental NGO, the Belize Blue Investment Company (BBIC), which is a subsidiary of TNC, and Credit Suisse (CS), referred to as the “middlemen” from now on. The deal assumed a tripartite model wherein the middlemen paid off the bondholders of the “Superbond 3,” which in 2021 was trading 40% below its face value and carried high default risk. On the secondary market, the bondholders were willing to accept the 40% discount because it was better than a default.

As a result, the Belize government’s debt fell by $363 million, but they agreed to a new, non-fixed 6% interest rate loan that would have to be paid back in 19 years. This critical step, which represents a profit opportunity for investors, was what allowed CS to raise funds to pay off the “Superbond 3” bondholders and assure investors. Since the DFNs were made in collaboration with the BBIC, through the Development Finance Cooperation, the US government promised to protect investors if the Belize government defaulted. This is in addition to $28 million that will be paid out to CS and TNC in legal and advisory fees.

Hence, the debt was restructured and not forgiven; however, $24 million was made available for a national marine trust fund in addition to a promise of $4 million in investment to the fund by the Belize government. This represents a direct investment in the country’s tourism industry which accounts for 40% of economic activity.

Bottom-line: You can’t eat the cake and have it. The DFN with the Belize government has unlocked new funds for environmental conservancy and prevented a looming default. However, the government is now on the hook for more debt, that it might not be able to repay.

* Please help my Economic Growth & Development students by commenting on unclear analysis, alternative perspectives, better data sources, or maybe just saying something nice :).

This is a very interesting blog post, because of the debt narrative which is very heavily used especially in the context of climate policies. I am currently taking macroeconomics, which revolves around the idea of public and private debt. According to the books we are reading, public debt is a myth and the main concerns we should have when it comes to financial and economic stability is controlling private debt. As it relates to your blog-post, I am curious about the issues you see in private loans taken out by companies to invest in sustainable technology, for example. The question ties into your point about what creditors stand to gain, which is something we should perhaps be more cautious of. All in all, this is a very interesting topic because it relates so much to the rhetorics governments have created around climate action. Much like we should rethink how we consume, I believe we should also rethink the way we view debt (particularly public debt).