Jacinta writes*

Jacinta writes*

Globe trotting has evolved from a luxury to an entitlement, largely enabled through a booming aviation market represented by uncharacteristically low prices. The industry was historically given the freedom to unfurl its wings, liberated by government subsidies through exemptions from VAT on tickets and fuel taxes [pdf], saving UK airlines approximately £10 billion annually.

This industry of substantial significance contributes to 8% of world GDP, 13% of the transport sectors GHG emissions and 2% of global GHG emissions. Masked by the benefits from net gains, the ‘only 2%’ argument has been tossed around a lot. Yet adhering to this train of thought would lead to a global paralysis, as many countries contribute to ‘only — or less than! — 2%’ of GHG emissions, such as the UK, Canada and Australia.

Carbon emissions aren’t the only cause for climatic concern. Due to the altitude at which emissions occur, aviation has more intense short lived impacts from contrails and cirrus clouds, resulting in high radiative forcing. Therefore, narrowing the timescale to a 5-year period, the aviation sector contributes more to global warming than all the cars on the road. This is a stark contrast to comparing only their GHG emissions (share of emissions within the transport sector: 13% aviation : 73% road). Couple this with the fast paced growth of the industry, and concern is brewing. According to the International Civil Aviation Organization (ICAO), by 2020, global aviation emissions are expected to exceed those of 2005 by 70%, with a further estimated growth of 300-700% by 2050. With this all in mind, questions arise over whether these short term impacts are careering us towards (and over) critical climate tipping points.

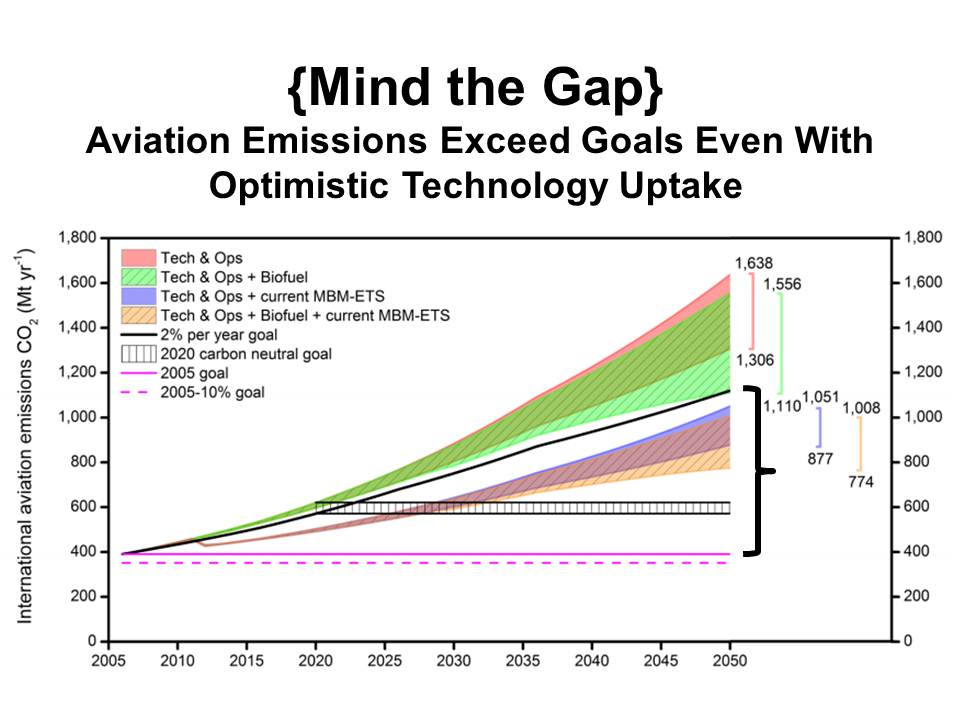

This complex issue is thus about more than carbon emissions, but action needs to occur, fast. The negative impacts from aviation are neither disputed nor (scientifically) underestimated, but it is one of the few industrial sectors with growing emissions. Technological efficiency has improved fuel efficiency by 70% over the years, but overall growth has outpaced emission reductions, and efficiency improvements will not come at the same rate as in the past. Although a must, promises of alternative fuels; claiming to enable continued growth without jeopardising climate change efforts, are considered fanciful. Therefore, further rapid expansion can not be compatible with the sustainability of the sector.

To date, the ICAO has been solely in charge of mitigation strategies. A challenging feat, being a globalised industry with differential treatment between developed and developing countries. However, results have been insufficient. Most recently, the ICAO 2016 proposal outlines offsetting future carbon emissions against a 2020 baseline, beginning with a voluntary opt-in participation by States. Critics have forecasted it will not be enough and that the “carbon neutral growth” goal will not be achieved:

Commentators voice the need for the use of market forces, taxation (whether that be a carbon and/or fuel tax) or stronger regulations, to enforce a stronger compliance to CO2 reduction and more stringent offsetting.

Bottom Line: Despite the technical advances reducing emissions per flight, the rapidly growing aviation sector shows no signs of slowing its contribution to climate change. Robust steps need to be taken to curb impacts.

* Please help my Environmental Economics students by commenting on unclear analysis, alternative perspectives, better data sources, or maybe just saying something nice :).